In May 2026, the Australian Government announced significant tax reforms affecting negative gearing, trusts and businesses as part of the Federal Budget.

In our Nexia Australia 2026 Federal Budget Insights report we provide a summary of the measures announced on 12 May 2026.

This article focuses on the proposed changes to negative gearing, which will limit losses for taxpayers acquiring residential dwellings from 1 July 2027.

Negative gearing – what does it mean?

Negative gearing occurs when the costs associated with an income-producing investment (such as a residential dwelling) exceed the income the residential dwelling generates.

Where a loss arises:

- The net loss can currently be offset against other income (such as salary and wages, business income or other investments) and reducing overall taxable income; and

- Depending on the taxpayers circumstances, this may result in a tax refund upon lodgment of a taxpayers tax return and assessment of the income tax for a year.

Under the current rules (prior to 30 June 2027), rental property losses can generally be used to offset against other forms of taxable income (e.g. salary and wages), which supports leveraged property investment.

What is changing?

On 28 May 2026, legislation was introduced into Parliament to amend the negative gearing rules for residential dwellings.

From 1 July 2027, the proposed rules will:1

- Limit the ability to use losses from residential dwellings; and

- Restrict these concessions primarily to new residential dwellings.

- Importantly, the tax rules introduce a new term for residential property – “residential dwelling” and which requires particular consideration by a residential property investor. For example, a residential property may not always be a residential dwelling (refer below).

These changes are expected to apply to individuals, partnerships, companies and most trusts.

These measures are contained in Treasury Laws Amendment (Tax Reform No.1) Bill 2026 (Cth) (Bill).

Why are these changes being introduced?

The tax policy intent is to encourage investment in new housing supply, while limiting tax benefits associated with established properties.

The Explanatory Memorandum to the Bill notes that the negative gearing (combined with the 50% capital gains (CGT) discount) can result in low or sometimes negative effective tax rates for dwelling investors.

These arrangements can create strong incentives for investors to take on highly leveraged housing investments, especially in established dwellings (as opposed to new residential dwellings).

The proposed changes aim to rebalance these outcomes by directing incentives towards increasing housing supply.

Treasury data indicates that approximately 1% of taxpayers acquire negatively geared properties each year (around 230,000 individuals in 2022-23).

At the time of this article, the measures described have not yet been passed into law.

This measure (and including the CGT reforms) are estimated to increase government revenue by $3.6 billion over the five years from 2025-26.

The general rule for loss quarantining – from 1 July 2027

From 1 July 2027, individuals, trusts and partnerships will be subject to new restrictions on the use of losses from residential dwelling investments.

Under the proposed rules, losses from negative gearing tax losses from residential dwellings will be quarantined, meaning the tax losses cannot be offset against other forms of income (such as salary and wages).

Quarantined losses can only be used to:

- Offset net income derived from residential dwellings used or held as residential accommodation; or

- Reduce capital gains or other income arising from a residential dwelling.

Any excess losses that cannot be utilised will be carried forward and can be applied against eligible residential dwelling income in future years.

Importantly:

- Eligible “new residential dwellings” will be excluded from the restrictions; and

- Investors in new residential dwellings can continue to offset net rental losses against other income (such as salary and wages), consistent with current treatment.

An example in the EM of the Bill provides,

“Henrietta acquires an established residential dwelling in July 2028.

For the 2028-29 income year Henrietta has assessable income of $50,000 from renting out the residential dwelling as residential accommodation.

For that year, Henrietta has $65,000 in deductions for the residential dwelling, including interest, insurance and strata costs. She can only deduct $50,000, and the remaining $15,000 is carried forward to the next income year.

For the 2029-30 income year, Henrietta has $70,000 in deductions and $52,000 of assessable income from renting out the residential dwelling as residential accommodation.

Henrietta can deduct $52,000, and $33,000 is carried forward to the next income year (comprising the $15,000 carried forward from the 2028-29 income year and $18,000 from the 2029-30 income year).

For the 2030-31 income year, Henrietta has $20,000 in deductions and $72,000 of assessable income from renting out the residential dwelling as residential accommodation, having reduced her mortgage following an inheritance.

She has net rental income from the residential dwelling of $52,000 for this income year and can fully offset the amount of $33,000 that has been carried forward from the previous income year.”

Other matters

Residential dwellings held within widely held trusts and superannuation funds will be excluded, along with targeted exemptions to be introduced via legislative instrument (yet to be issued). These are expected to include build-to-rent developments and private investors supporting government housing programs (refer 2026 Budget Paper No. 2, page 21).

These rules will generally apply to interests in residential dwellings acquired on or after 7.30pm (AEST) on 12 May 2026, unless an exception applies.

Residential dwellings acquired prior to 7:30pm (AEST) on 12 May 2026 (including contracts entered into but not yet settled) will be exempt from these changes until disposal.

Other investments

The loss quarantining rules do not apply to other asset classes such as shares or commercial dwelling.

Investors can continue to deduct all losses and outgoings from these investments against other forms of assessable income (e.g. salary and wages).

Exempt residential dwelling acquisitions – prior to AEST 7.30pm (AEST) on 12 May 2026

Investments made prior to 7.30pm (AEST) on 12 May 2026 are also exempt from the loss quarantining rules. This ensures that taxpayers who made investment decisions under the existing regime are not impacted retrospectively.

Meaning of residential dwelling

The meaning of the term “residential dwelling” requires some consideration and is a term defined in the new tax rules.

For the loss quarantining rules to apply, the investment must be related to a residential dwelling used or held as residential accommodation.

A ‘residential dwelling’ is a dwelling which is defined as

- A unit of accommodation that:

- is a building or is contained in a building; and

- consists wholly or mainly of residential accommodation.

A ‘residential dwelling’ also includes, where available for use by the occupant:

- land adjacent to the dwelling; and

- a garage, storeroom or other associated structure.

(Refer proposed section 26-160(1) as further defined in section 118-115 of the ITAA 1997, and which, as currently drafted, creates a difference between the term dwelling for negative gearing and for purposes of the principal place of residence in Division 118 of ITAA 1997.)

A residential dwelling includes detached and semi-detached houses, units, apartments and townhouses.

There is no restriction based on how long the dwelling is occupied. For example, properties used for short-term stays may still qualify where they are suitable for residential accommodation.

Where a dwelling is used partly as a main residence and partly as to generate rental income, deductions must be apportioned. Only the portion relating to the income-producing use will be deductible.

What is not a residential dwelling

A residential dwelling is not:

- a Caravan, mobile tiny home or similar mobile structure;

- a Hotel, motel, inn, hostel, or boarding house;

- a Student accommodation connected to an educational institution;

- a Boat or other marine vessels; or

- Any other class of dwelling excluded by legislative instrument.

Interests acquired before 12 May 2026

The tax loss quarantining rules do not apply to the following interests:

- Residential dwelling held at 7.30pm (AEST) on 12 May 2026;

- Vacant residential land held at 7.30pm (AEST) on 12 May 2026; or

- Land where a residential dwelling is being built or is contracted to be built, and the completion of construction occurs after 7.30pm (AEST) on 12 May 2026.

Where construction has commenced (including demolition or rebuilding) before this time, the new rules are not expected to apply to that dwelling. However, other tax rules (e.g. vacant land holding cost rules) may still limit deductions.

Main residence – owned on or before 12 May 2026

Where dwelling held as a main residence at 12 May 2026 is subsequently rented, the application of these rules remains uncertain. Based on current guidance, such properties may not be impacted, however further clarification is expected and despite the following example in the Bill.

An example at para 2.37 of the Explanatory Memorandum,

“Example 2.4 Ownership interest in an established dwelling pre-12 May 2026

Maya acquired an ownership interest in a residential dwelling prior to 7.30pm (AEST) on 12 May 2026 (Dwelling A). This dwelling is her main residence and is subject to a home loan for which she pays interest and makes principal repayments.

On 25 August 2029, Maya moves to another city and seeks to rent the apartment. On 1 September 2029, Maya advertises Dwelling A for rent and rents Dwelling A to a tenant.

For the 2029-30 income year, Maya is able to claim deductions, such as interest paid on the loan for Dwelling A, against her assessable income, including her salary and wages, for the period 1 September 2029 to 30 June 2030.”

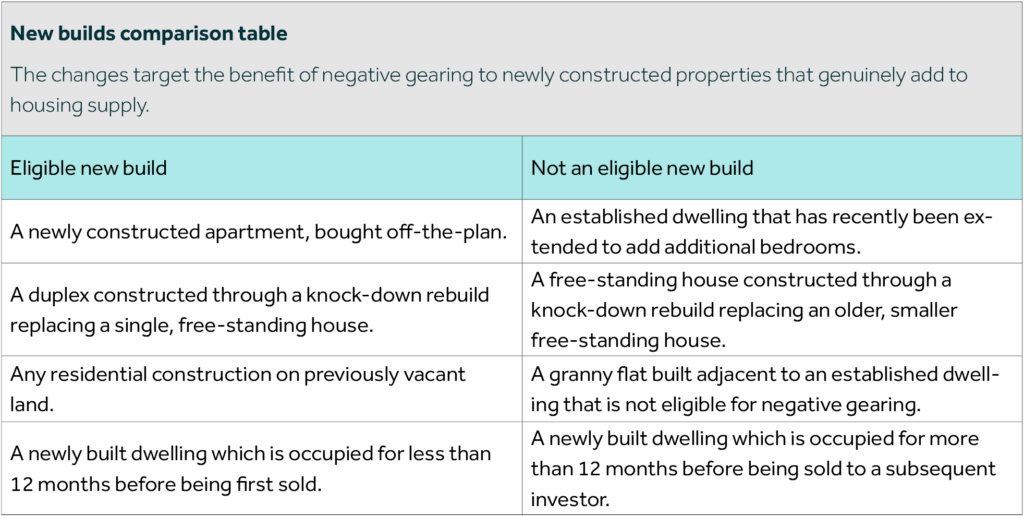

Meaning of new residential dwelling

Negative gearing losses incurred in relation to new residential dwellings from 1 July 2027 will continue to be deductible.

The policy intent behind this approach is to ensure that the benefits of negative gearing are directed towards investments that genuinely increase housing supply in Australia.

A residential dwelling will be considered a ‘new residential dwelling’ where it meets the requirements determined by the Minister through legislative instrument.

At the time of this publication, this legislative instrument outlining the detailed definition has not yet been released by the Government.

As part of the 12 May 2026 Federal Budget, the Government provided further guidance in its factsheet, noting that:

“New builds are residential properties which genuinely add to supply (see Table 2). This will include:

- dwellings constructed on vacant land, or

- where existing properties are demolished and replaced with a greater number of dwellings.

Knock-down rebuilds or substantial renovations that do not increase supply will not be eligible.

A new build cannot have been previously sold, unless first owned by the builder and not occupied for more than 12 months.

Subsequent purchasers of the dwelling will not be able to access the 50 per cent CGT discount or negative gearing in relation to that dwelling. This is similar to how stamp duty exemptions apply to new builds under some state-based arrangements.

Refer to “Negative Gearing and Capital Gains Tax Reform” Treasury Factsheet dated 12 May 2026.”

Until the above policy disclosures made in the May 2026 Federal Budget are made, the above definition of “new residential dwelling” remains unclear.

Other exemptions

The proposed changes to negative gearing apply only to residential dwellings. Other asset classes, such as commercial properties and shares, will continue to be subject to existing tax arrangements.

In addition, further exemptions are expected to apply for private investors supporting government housing initiatives, including affordable housing programs and per legislative instruments to be issued by the Government.

Modification in relation to beneficiaries of trusts

There are also some specific trust related measures and whereby the above loss quarantining rules are modified in relation to beneficiaries of trusts.

- This modification ensures that the character of trust income flows through to beneficiaries. This allows beneficiaries to apply trust income – where it relates to residential income – against any losses they may have from quarantined residential dwellings.

- This approach ensures that beneficiaries are not adversely impacted where a trust distributes net income derived from residential dwelling. The rules also allow the look-through approach to apply through interposed partnerships and trust structures.

- Similarly, where an entity borrows to acquire an interest in a unit trust, the interest costs on that borrowing will be subject to the general loss quarantining rules where the unit trust holds residential dwelling and distributes income to the entity. (Refer section 26-155(7) of the ITAA 1997)

These measures form part of the broader proposed changes to negative gearing in Australia from 1 July 2027.

Next steps

Given the proposed changes to negative gearing, it is important to consider how these rules may apply to your current or planned property or residential dwelling investments. In particular:

- Reviewing your existing residential dwelling portfolio, including the timing of acquisitions.

- Reviewing the new definition of “residential dwelling” and general concept of residential property, noting commercial properties and industrial properties are excluded from the above rules.

- Considering how the proposed loss restrictions may impact your after-tax position and cash flow.

- Assessing whether future investment strategies (including new vs established properties) remain appropriate.

- Seeking tailored advice before making any investment or restructuring decisions.

As these measures are still in draft form, we will continue to monitor developments and provide updates as further details become available.

If you have any questions about any of the Budget announcements and what they mean for you or your business, talk to your trusted Nexia Advisor.

[1] 2028 Federal Election Assumption – While speculation, for the purposes of this publication, and given the proposed operation date of the above rules from 1 July 2027, we have assumed the Australian Labour Party will win the next Australian Federal Election on or before May 2028 and there will be no changes to these tax rules from say 1 July 2028. Given this 2028 Federal Election Assumption and the presence of some uncertainty, we advise the contents of this publication is not a substitute for obtaining tax advice based on your personal circumstances.