Snapshot for the FBT year ending 31 March 2026

FBT rate: 47%

Type 1 gross-up rate: 2.0802

Type 2 gross-up rate: 1.8868

Benchmark interest rate: 8.62%

Car parking threshold: $11.03 daily

Record-keeping exemption: $10,664

Timing: FBT return is due by 21 May 2026, or 25 June 2026 if lodged electronically through your tax agent.

Why does FBT exist?

Fringe Benefits Tax (FBT) is a tax imposed on employers for certain non-cash benefits provided to employees, associates and related parties. Its purpose is to prevent tax leakage where an employer claims a tax deduction for providing benefits, but the employee does not pay income tax on the value received.

Common types of fringe benefits provided by NFP organisations

- Motor vehicles

- Meal entertainment

- Housing

- Living away from home allowance (LAFHA)

- Residual benefits (e.g. discounted school fees)

- Other property and expense fringe benefits

NFP employer categories and concessional FBT treatment

Not-for-profit (NFP) employers may access concessional FBT treatment, but the type of concession depends on their ATO endorsement status.

There are two main categories:

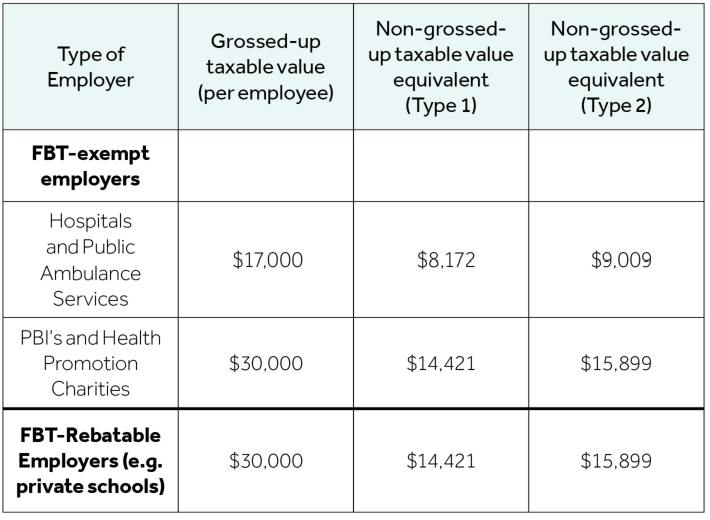

1. FBT-exempt employers

ATO-endorsed employers such as Public Benevolent Institutions (PBIs), health promotion charities, public hospitals, and public ambulance services can provide certain fringe benefits that are exempt from FBT up to an annual cap per employee under section 57A of the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986).

- Public hospitals and ambulance services: $17,000 grossed-up cap per employee

- PBIs and health promotion charities (non-hospital): $30,000 grossed-up cap per employee

If the grossed-up value of benefits exceeds the relevant cap, FBT is payable on the excess.

2. FBT-rebatable employers

Certain NFP organisations (such as registered charities that are not PBIs or health promotion charities, scientific institutions, public educational institutions, and specific societies or clubs) are entitled to a rebate on the FBT otherwise payable, rather than a full exemption. The rebate reduces the FBT liability up to a capped amount of benefits per employee (generally $30,000 grossed-up value).

Capping thresholds for the 2026 FBT year

General fringe benefits caps

Eligible employers can provide fringe benefits that are either exempt (for FBT-exempt entities) or eligible for a rebate (for rebatable entities) up to these caps on a per-employee, per-FBT-year basis.

Examples:

FBT-exempt employer

- If the total grossed-up value of car fringe benefits provided to an employee is $28,000, no FBT is payable. If the total grossed-up value is $35,000, FBT is payable only on the excess $5,000.

FBT-rebatable employer

- If the total grossed-up value of the car fringe benefits provided to an employee is $35,000, the FBT rebate can only be claimed on the FBT liability relating to the first $30,000 of grossed-up benefits provided to the employee. The rebate ($6,627) is calculated as a percentage (currently 47%) of the FBT payable on the eligible capped amount (i.e. $30,000 x 47% x 47%). For the FBT liability relating to the excess $5,000 (i.e. $35,000 – $30,000), no rebate is available, and the employer must pay the full FBT on this amount.

It is important to note that the rebate is not apportioned for part-year employment. An employee who commences on 1 January 2026 is still entitled to the full annual cap. Any unused cap amount cannot be carried forward to a later year and cannot be transferred to another employee.

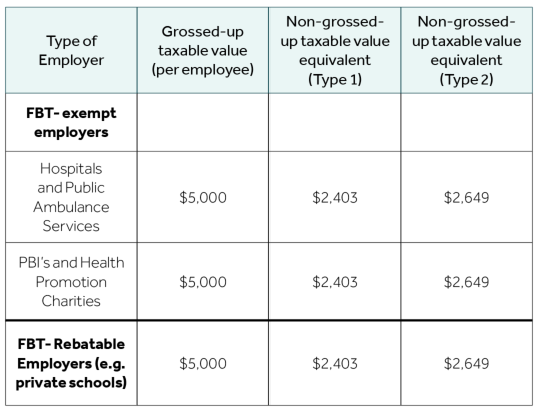

Salary-packaged meal entertainment

A separate $5,000 grossed-up cap per employee applies to salary packaged meal entertainment and entertainment facility leasing expenses for both FBT-exempt and FBT-rebatable employers. This is equivalent to $2,403 on a Type 1 basis or $2,649 on a Type 2 basis.

Examples:

FBT-exempt employer:

- Benefits within the $5,000 grossed-up cap are exempt from FBT and do not count towards the general $30,000 exemption cap. Any amount above $5,000 is included in the calculation of the general cap. For example, if an employee salary packaged meal entertainment with a grossed-up value of $2,649 using the Type 2 rate, the amount is fully exempt. If the grossed-up value exceeds $5,000, the excess is counted towards the $30,000 exemption cap.

FBT-rebatable employer:

- The same $5,000 grossed-up cap applies when determining the amount eligible for the rebate. Benefits within this cap are eligible for the rebate, while any excess is included in the calculation of the general $30,000 rebate cap per employee.

Meal entertainment (non-salary packaged)

Meal entertainment, for FBT purposes, refers to entertainment provided through food or drink, along with any related accommodation or travel. This can include restaurant meals, social functions, Christmas parties, and expenses like taxis to and from a venue. It applies even if business discussions occur and also covers benefits provided to employees’ spouses or associates.

Meal entertainment can be valued using the actual method or the 50/50 split method. The actual method is generally more tax-effective when most entertainment is for non-employees as only the portion provided to employees is subject to FBT. The 50/50 split method may be preferable when most entertainment is for employees, applying FBT to half the total expenditure and simplifying record-keeping.

Religious practitioners

A private school registered with the ACNC under the subtype ‘advancing religion’ may qualify as a religious institution for FBT purposes. If the school employs staff who are religious practitioners, such as ordained ministers or chaplains performing predominantly religious duties, certain benefits provided to those employees can be exempt from FBT under section 57 of the FBTAA 1986. The exemption only applies where the employee meets the definition of a religious practitioner and the benefits are provided in respect of their pastoral or religious activities.

Car parking

Registered charities, scientific institutions (that are not carried on for the purposes of profit or gain to individual shareholders or members), and public educational institutions are generally exempt from FBT when providing car parking fringe benefits to employees. This exemption applies whether the benefit is provided as a car parking benefit or as an eligible car parking expense payment benefit, provided the relevant eligibility criteria under section 58G of the FBTAA 1986 are satisfied.

Some general exemptions from FBT

In addition to the concessional treatment available to NFP employers, a number of fringe benefits are exempt from FBT for all employers, provided certain conditions are met:

Portable electronic device: One work-related portable electronic device (e.g. laptop, tablet, mobile phone) per employee per FBT year is exempt, provided it is primarily used for employment purposes. Additional devices may be exempt if they are replacements or, for small businesses, if provided after 1 April 2021.

Minor benefits: Benefits with a value of less than $300 (GST inclusive) that are provided infrequently and irregularly are exempt. This does not generally include meal entertainment for income tax-exempt organisations.

Otherwise deductible expenses: If the employee would have been entitled to an income tax deduction for the expense had they incurred it themselves, the benefit is exempt from FBT.

Electric Vehicles: Zero or low emissions vehicles may be exempt from FBT where all legislative conditions are satisfied. From 1 April 2025, plug-in hybrid electric vehicles are no longer eligible for the exemption unless there was a financially binding commitment in place before that date to continue providing the vehicle for private use.

Reportable fringe benefits

Where the taxable value of certain fringe benefits provided to an employee exceeds $2,000 in an FBT year, the grossed-up amount must be reported on the employee’s PAYG payment summary. The minimum grossed-up value is $3,773 (being $2,000 multiplied by the Type 2 gross-up rate). Although employees do not pay income tax on this amount, it is included in the calculation of various means-tested benefits and obligations, such as:

- Liability to the Medicare levy surcharge

- Child support payments and benefits

- Recovery of HELP debt (previously known as HECS)

- Income tests for youth allowance, family tax benefit and childcare benefit

- Personal and spouse’s super contribution rebate

If the fringe benefits provided by a NFP employer to an employee are below the relevant exemption thresholds, they do not need to be reported on the PAYG payment summary.

Think about the possibilities in your organisation

As you work through your 2026 FBT compliance, it is worth considering the options available within your organisation for the coming year. Reviewing benefit structures and salary packaging arrangements can help ensure you maximise available concessions while remaining compliant.

Our team at Nexia can work with you to explore appropriate strategies, address any questions, and provide practical guidance to help you and your employees achieve the best outcomes.

FBT Year End Planner - For-purpose (Not-for-profit)

Download PDF