In August 2025, the High Court of Australia handed down a much-anticipated decision in FCT v PepsiCo [2025] HCA 30 (13 August 2025), involving Australian royalty withholding tax and the Australian Diverted Profits Tax.

Facts

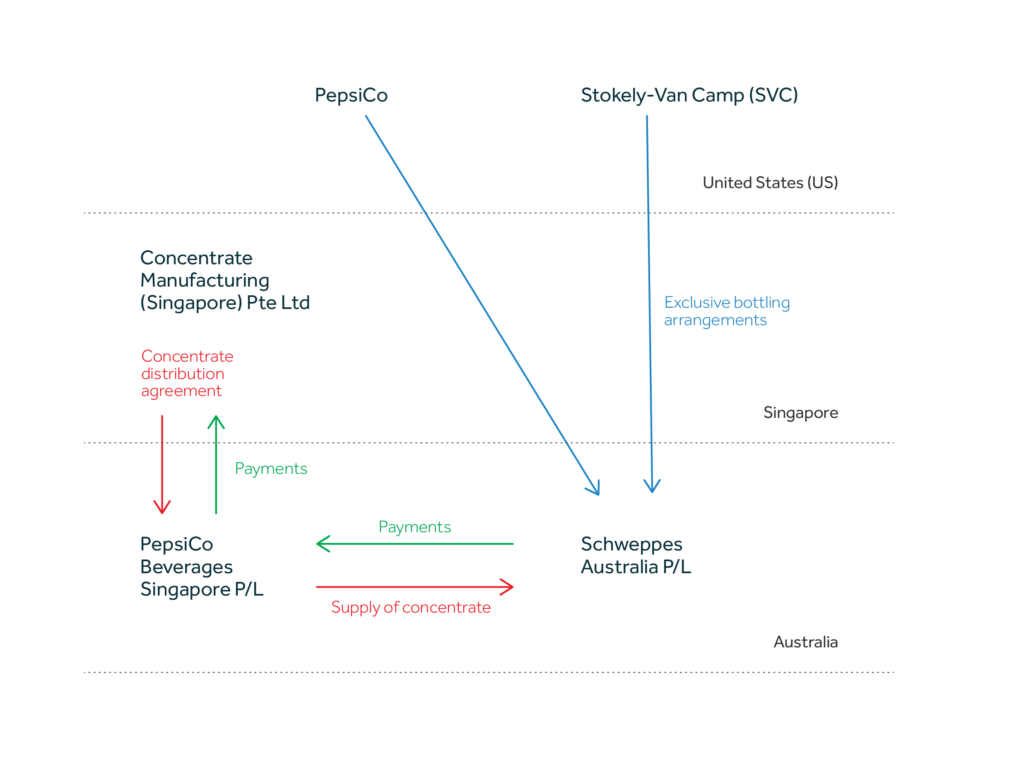

The following companies in the PepsiCo group were involved in bottling and distribution of PepsiCo and other soft drinks in Australia:

- PepsiCo Inc (US) (PepsiCo), a US-listed multinational corporation.

- PepsiCo, which includes Stokely-Van Camp Inc (SVC), another US company.

- PepsiCo Bottling Singapore Pty Ltd (Seller) an Australian company and part of the PepsiCo (US) group.

- Concentrate Manufacturing (Singapore) Pte Ltd, a Singapore company that manufactured and distributed soft drink concentrate.

The above businesses entered the following interrelated contractual agreements:

From 1 July 2017 to 30 June 2019, Schweppes Australia Pty Ltd (Schweppes P/L) was the exclusive distributor and bottler of Pepsi, Mountain Dew and Gatorade in Australia. Schweppes was a company independently owned by Asahi Breweries.

Schweppes P/L purchase soft drink concentrate from PepsiCo Bottling Singapore Pty Ltd, under “Exclusive Bottling Arrangements” (EBAs) with invoices reflecting concentrate rates plus freight, insurance and handling fees.

Under the EBA executed in 2009, the US companies were to sell or cause another member of the PepsiCo group to sell to Schweppes P/L the concentrate it needed to make branded drinks.

The EBAs set out the prices of the relevant concentrates. The EBAs:

- Also included a grant by PepsiCo / SVC of the right to use the trade marks and other intellectual property associated with the soft drink beverages, such as can and bottle designs.

- The Pepsi EBA implied the grant by law and the SVC EBA specifically provided a license to use the designs.

- Under the EBAs, there were strict terms for the use of the trademarks and further requirements relating to testing and inspection of bottling facilities.

After the execution of the EBAs, PepsiCo notified Schweppes P/L that the seller of the units of the concentrate would be PepsiCo Beverages Singapore P/L (PepsiCo Beverages), an Australian resident company.

On 1 January 2018, a Singapore company, Concentrate Manufacturing (Singapore) Pte Ltd (and a member of the PepsiCo group) and PepsiCo Beverages entered into a concentrate distribution agreement.

As part of the tax dispute,

- The Australian Taxation Office (ATO) issued notices of royalty withholding tax to PepsiCo and SVC, totaling A$3.6 million (refer to section 128B of the Income Tax Assessment Act 1936 (Cth) (ITAA 1936) and Article 12 of the Australian / United States Double Tax Agreement.

- In the alternative, the ATO issued Diverted Profits Tax assessments applying Part IVA and imposing A$28.9 million in additional tax for the relevant years.

Full Federal Court

In 2024, the Full Federal Court of Australia held,

- The payments were not income of PepsiCo and SVC and no payments under the EBA were subject to Australian royalty withholding tax as there was no royalty for the use of PepsiCo / SVC’s intellectual property.

- The payments did not give rise to Diverted Profits Tax provisions as PepsiCo did not obtain a tax benefit in connection with a scheme.

High Court – August 2025

In August 2025, the High Court dismissed the ATO appeal. The High Court held PepsiCo and SVC were not liable to Australian royalty withholding tax. The amounts paid by SAPL to PBS for concentrate were not ‘consideration for’ the use of the PepsiCo intellectual property (at para [174]).

The High Court also held PepsiCo and SVC were not liable to the Australian Diverted Profits Tax. Under the EBAs and related events, PepsiCo and SVC did not obtain a tax benefit under the Divert Profits Tax anti-avoidance rules and pursuant to section 177D of the ITAA 1936 (at para [237]).

Takeaway

Since the Full Federal Court decision on 26 June 2024, the ATO have also issued views in respect of royalty withholding tax, including the views in TR 2024/D1 [Income tax: royalties – character of payments in respect of software and intellectual property rights] and PCG 2024/1 [Intangibles migration arrangements].

Sometime after 13 August 2025, we anticipate the ATO to release a Decision Impact Statement outlining the ATO’s perspective on the practical implications of the above loss in the High Court. It would also address how the High Court’s decision influences the ATO’s current stance on the inbound company’s liability for Australian royalty withholding tax.

Next steps

Please contact your Nexia advisor if you require any professional tax advice in relation to the above matters, and whether cross-border transactions involving intellectual property rights under inter-company agreements gain great scrutiny by the ATO, given the recent High Court decision in PepsiCo.