Treasurer Jim Chalmers has delivered his fifth Federal Budget (Budget), introducing significant tax reforms to property, trust and business taxation in Australia.

The 2026/27 Budget aims to provide relief to individuals while allowing businesses to grow in an uncertain inflationary environment. It also proposes significant changes to property taxes and trust taxation to strengthen Australia’s fiscal policy.

Our team at Nexia Australia set out a summary of the key measures announced, and what they may mean for you and your business.

2026/27 Federal Budget summary contents

Contents: Scroll to Personal tax / Scroll to Negative gearing and Capital gains tax / Scroll to 30% tax on discretionary trusts / Scroll to Business tax / Scroll to International tax

Personal tax

Income tax rates

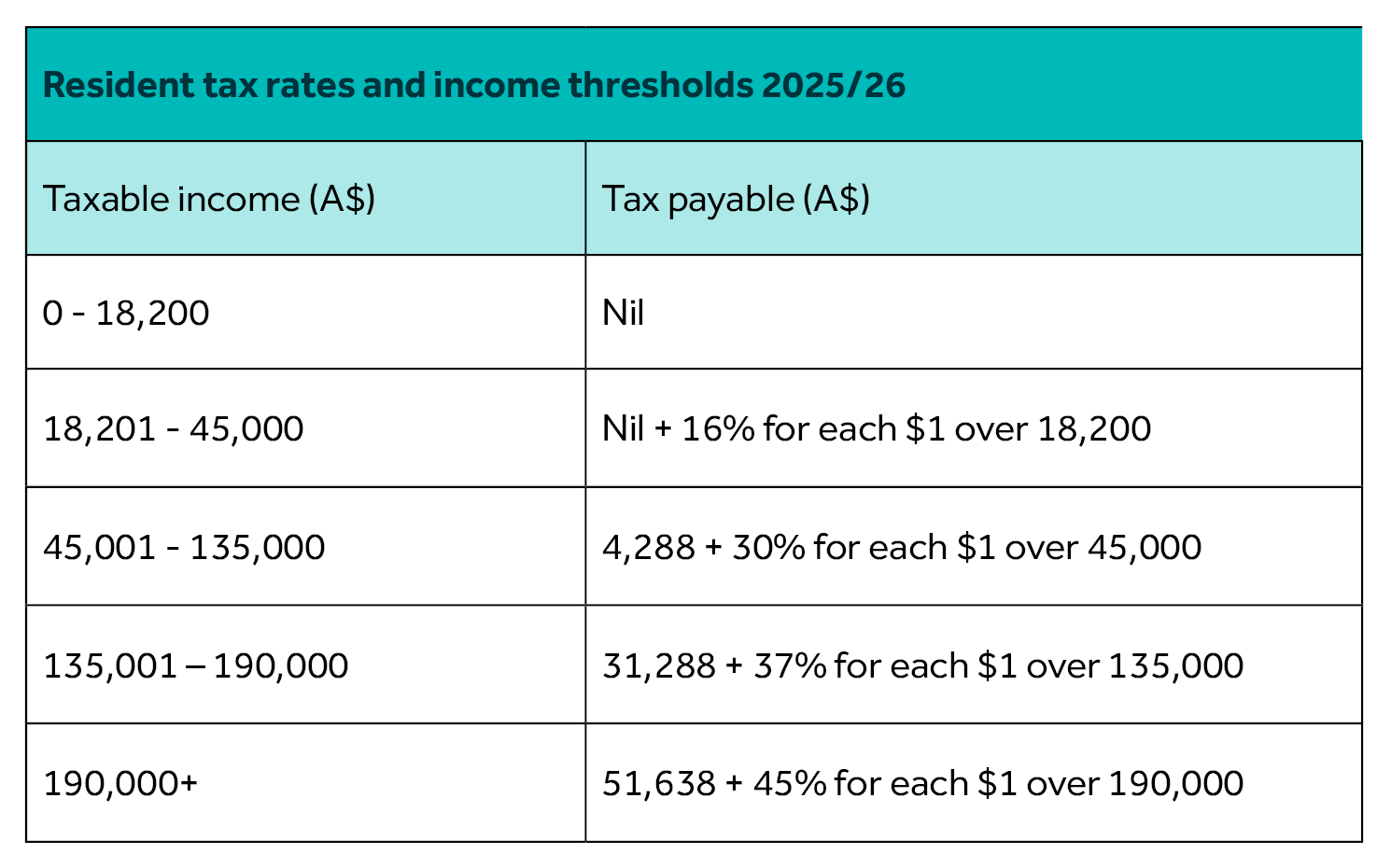

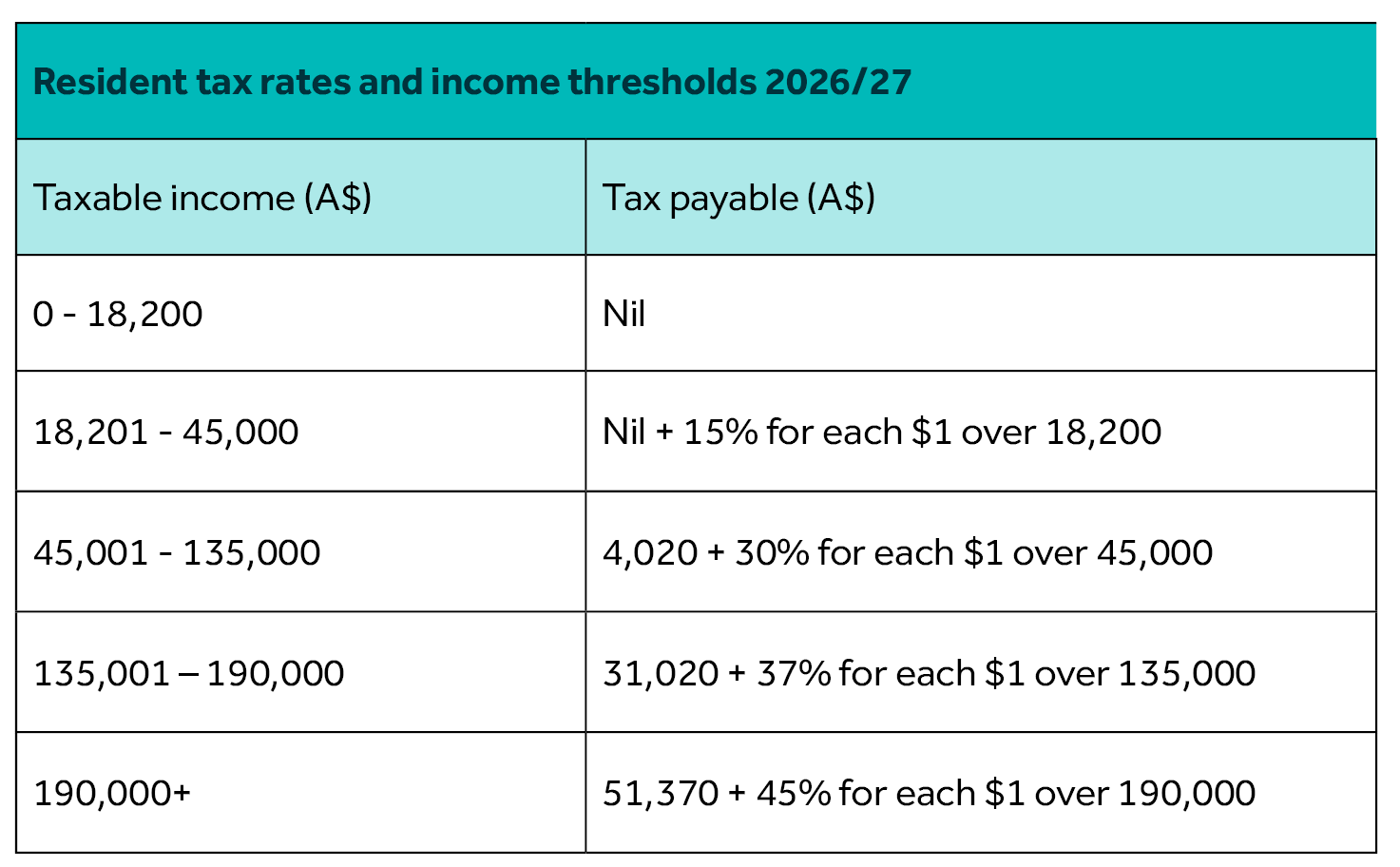

There were no changes announced for tax rates applying in Financial Year (FY) 2025/26 and FY 2026/27.

Resident tax rates and thresholds for FY 2025/26

The FY 2025/26 tax rates and income thresholds for residents remain unchanged and are as follows:

The Medicare levy low-income thresholds for singles, families, and seniors and pensioners will increase by 2.9% from 1 July 2025.

The FY 2026/27 tax rates and income thresholds for residents remain unchanged and are as follows:

Working Australian Tax Offset – 2027/28 income tax year

For the 2027-28 income tax year, a tax cut for every working Australian taxpayer was introduced via a $250 Working Australians Tax Offset.

New standard deduction of $1,000 for individuals – proposed change to deductions

A new standard deduction of $1,000 will apply for certain individual taxpayers who mainly derive salary and wage income for the first financial year 1 July 2026 to 30 June 2027.

Taxpayers with more than $1,000 in deductions in the year ending 30 June 2027 may continue to itemise and substantiate their claims in line with existing rules. If a taxpayer has incurred more than $1,000 in deductions, the taxpayer’s standard deduction is reduced to zero.

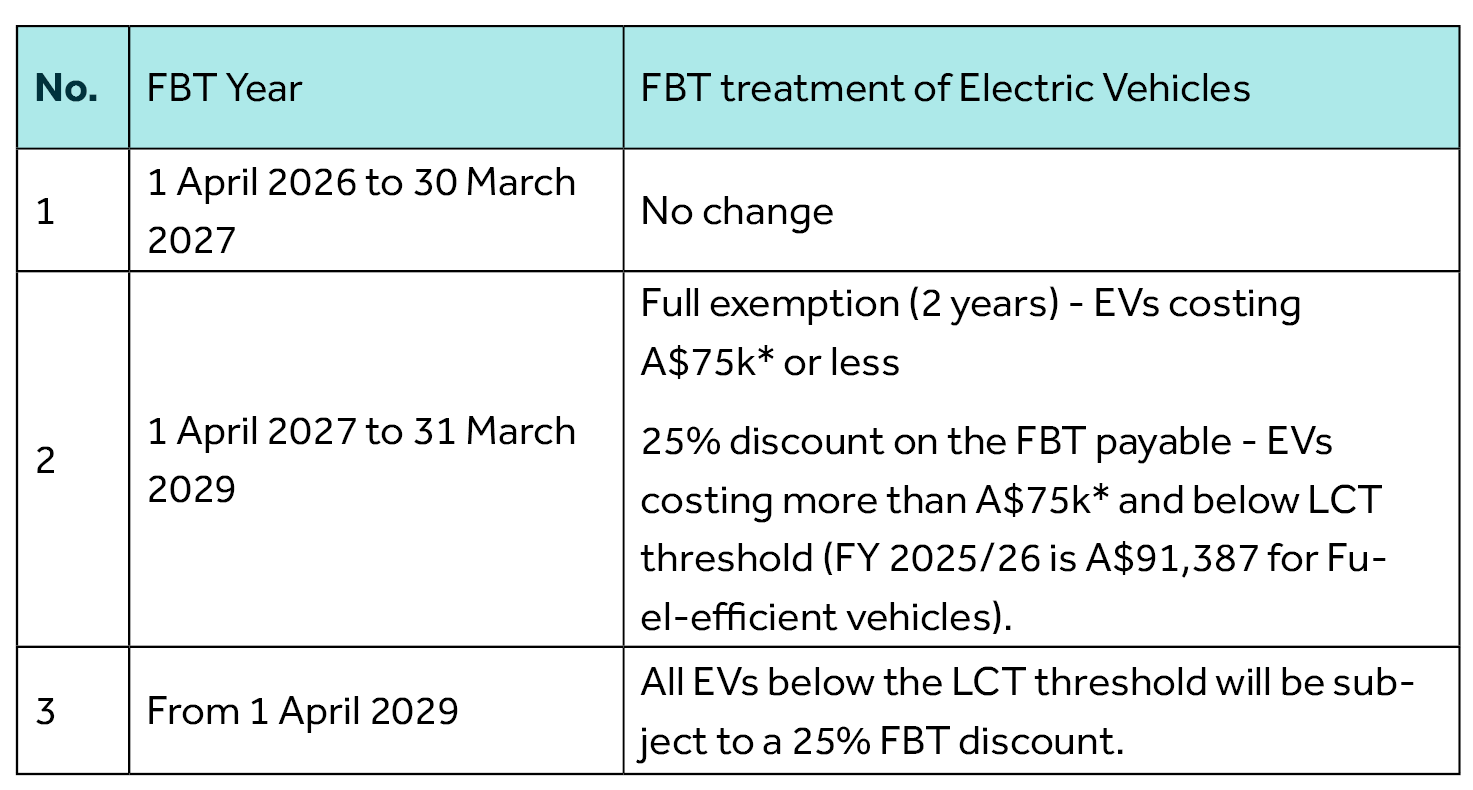

Fringe Benefits Tax (FBT) – Transition to 25% FBT discount for certain Electric Vehicles

The FBT exemption that applies to Electronic Vehicles (EV) provided by employers to employees is reduced on the following basis:

*GST exclusive

All eligible EVs will retain the FBT discount rate that was in place when the arrangement commenced;

The existing 20 per cent statutory rate will continue to apply for all other cars, including electric cars costing more than the fuel-efficient luxury car tax threshold.

Reportable fringe benefits will continue to be determined for eligible electric cars as if a 20 per cent FBT statutory formula rate or operating cost basis method applied.

Negative Gearing and Capital Gains Tax (CGT)

Capital Gains Tax

The Government is reforming capital gains tax (CGT) arrangements to improve the fairness of the tax system, support home ownership and help fund new tax cuts for workers.

Improving Tax Arrangements for Capital Gains – From 1 July 2027, the 50 per cent CGT discount will be replaced by cost base indexation for assets held for more than 12 months, with a 30 per cent minimum tax on net capital gains. These changes will apply to all CGT assets, including pre-1985 CGT assets, held by individuals, trusts and partnerships.

Transitional arrangements will limit the impact on existing investments by ensuring the changes only apply to gains arising on or after 1 July 2027.

The 50 per cent CGT discount will continue to apply to gains arising before 1 July 2027.

Capital gains on pre-1985 assets arising before 1 July 2027 will remain exempt from CGT.

To maintain incentives for new housing supply, investors in new residential properties will be able to choose either the 50 per cent CGT discount, or cost base indexation and the minimum tax. Income support payment recipients, including Age Pension recipients, will be exempt from the minimum tax.

Negative Gearing

Reforming Negative Gearing to Support New Housing Supply – The Government will limit negative gearing for residential property to new builds.

From 1 July 2027, losses from established residential properties will only be deductible against rental income or the capital gains from residential properties. Excess losses will be carried forward and able to be offset against residential property income in future years.

These changes will apply to established residential properties acquired from 7:30PM (AEST) on 12 May 2026. Properties acquired prior to this time (including contracts entered into but not yet settled) will be exempt from the changes until disposed of.

Eligible new builds will be exempt from the changes, ensuring the benefits of negative gearing are directed to investment that increases the housing stock. Properties in widely held trusts and superannuation funds will be excluded, alongside targeted exemptions for build-to-rent developments and private investors supporting government housing programs.

This measure is estimated to increase receipts by $3.6 billion over the five years from 2025/26.

30% minimum tax on discretionary trusts

From 1 July 2028, the Government will introduce a 30 per cent minimum tax on discretionary trusts to improve the fairness of the tax system and help fund new tax cuts for workers.

From 1 July 2028, trustees will pay a minimum tax of 30 per cent on the taxable income of discretionary trusts. Beneficiaries, other than corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee.

The minimum tax will not apply to other types of trusts such as fixed and widely held trusts (including fixed testamentary trusts), complying superannuation funds, special disability trusts, deceased estates and charitable trusts.

Corporate beneficiaries – Trusts can distribute to corporate beneficiaries that have access to corporate tax rates and franking credits, and which can be used to defer tax for underlying shareholders, who are often also trust beneficiaries. Under the minimum tax, corporate beneficiaries will be assessed based on the trust income to which they are entitled, without being able to claim credits for tax payable by the trustee. This will ensure the minimum tax cannot be avoided by cycling income through a ‘bucket’ company (Refer “Minimum tax on discretionary trusts” [dated 12 May 2026] on the Federal Government Budget website).

In addition, some types of income such as primary production income, certain income relating to vulnerable minors, amounts to which non-resident withholding tax applies, and income from assets of discretionary testamentary trusts existing at announcement will also be excluded.

Rollover relief will be available to assist small businesses and others that wish to restructure out of a discretionary trust into other arrangements, such as a company or a fixed trust. This will provide expanded relief from income tax consequences, including capital gains tax, for those who choose to restructure, and will be available for three years from 1 July 2027 (Refer “Minimum tax on discretionary trusts” [dated 12 May 2026] on the Federal Government Budget website). State taxes and state duties will require consideration.

A further Nexia publication will address the above measures in more detail, given proposed consultation with stakeholders.

This measure is estimated to increase receipts by $4.5 billion over the five years from 2025/26.

Business tax

$20,000 instant asset write-off

The Government has announced that the $20,000 instant asset write-off threshold for small businesses with aggregated turnover below $10 million will become a permanent feature of the tax system.

Without this change, the threshold was scheduled to revert to $1,000 from 1 July 2026.

The permanent extension is intended to provide greater certainty for small businesses undertaking equipment purchases and capital expenditure planning.

Assets above the threshold will continue to be allocated to the simplified depreciation pool.

The temporary suspension of the five-year restriction on re-entering the simplified depreciation regime after opting out will continue until 30 June 2027.

Loss refundability for businesses and start-up businesses

The Government will provide tax relief to businesses and start‑ups by reforming the treatment of tax losses. This will encourage investment and sensible risk‑taking and improve the resilience of firms through temporary shocks.

- Businesses – For tax years commencing on or after 1 July 2026, companies with aggregated annual global turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. Loss carry back will apply to revenue losses only and will be limited by a company’s franking account balance.

- Start-up companies – The Government will also introduce loss refundability for small start‑up companies. For tax years commencing on or after 1 July 2028, start‑up companies with aggregated annual turnover of less than $10 million that generate a tax loss in their first two years of operation will be able to utilise the loss to generate a refundable tax offset. The offset will be limited to the value of fringe benefits tax and withholding tax on wages paid in respect of Australian employees in the loss year.

Research and development tax offset

The Government is reforming the Research and Development Tax Incentive (R&DTI) to simplify and better target Government support for business R&D. From 1 July 2028, the Government will:

- Increase the offset for core R&D expenditure by around 25 to 50 per cent, through a 4.5 percentage point increase in core R&D offset rates;

- Reduce the intensity threshold from 2 per cent to 1.5 per cent, enabling more firms that engage in substantial core R&D to qualify for higher offset rates;

- Remove eligibility of supporting R&D expenditure for the R&DTI;

- Enable growing firms to retain access to the refundable tax offset for longer by increasing the turnover threshold for the highest offset rate from $20 million to $50 million;

- For firms below the $50 million turnover threshold, maintain older firms’ eligibility for the higher offset rate while limiting refundability to firms under 10 years of age;

- Lift the maximum R&DTI expenditure threshold from $150 million to $200 million; and

- Improve assurance on smaller claims by lifting the minimum expenditure threshold from $20,000 to $50,000, with research activities valued below this amount required to be undertaken with a registered Research Service Provider or Cooperative Research Centre to be eligible for the R&DTI. Nexia Comment: these measures represent a significant change to how some very small businesses may access the R&DTI.

- The Australian Taxation Office will receive $2.8 million in funding over three years from 2027–28 to support implementation of the measure, to be held in the Contingency Reserve pending finalisation of administrative arrangements.

The above measure forms part of the first stage of the Government’s response to the Ambitious Australia: Strategic Examination of Research and Development Final Report (March 2026).

Expanding venture capital tax incentives

The Government will expand the venture capital tax incentives to better facilitate venture capital investment and support early stage and growth businesses. From 1 July 2027:

- The venture capital limited partnership (VCLP) cap on the asset size of the investee business at the time of investment will be increased to $480 million, from $250 million;

- The early stage venture capital limited partnership (ESVCLP) cap on the asset size of the investee business at the time of investment will be increased to $80 million, from $50 million;

- The ESVCLP tax incentive cap on the asset size of the investee business, at which investment returns can be fully tax exempt, will be increased to $420 million, from $250 million; and

- The maximum fund size of ESVCLPs will be increased to $270 million, from $200 million.

The increases will apply to new and existing funds and to new investments they make, including where funds make further investments in businesses already held. ESVCLPs must remain in compliance with their existing investment plans or seek approval for a replacement plan.

The eligible venture capital investor program will be closed to new applications from 7.30PM (AEST) 12 May 2026.

PAYG instalment pilot for small and medium sized businesses

The Australian Taxation Office will expand its pilot of dynamic pay as you go (PAYG) instalment calculation to permit monthly payments.

From 1 July 2027, small and medium businesses will be able to opt in to reporting and paying PAYG instalments monthly and to using an ATO-approved calculation embedded in accounting software to calculate and vary their instalments.

This will support businesses by enabling tax instalments to better reflect real time business activity.

Taxpayers with a demonstrated history of non‑compliance will be required to report and pay PAYG instalments monthly.

International tax

The Budget contains limited international tax reform measures. However, the Government has announced amendments to Australia’s global and domestic minimum tax framework, amendments to the foreign resident capital gains tax regime and additional reforms to Australia’s foreign investment framework.

Changes to foreign resident CGT regime

The Budget has announced the following changes to the foreign resident capital gains tax regime and the disposal of CGT assets:

- Amendments to the definition of taxable Australian real property (TARP), including a statutory definition of real property. TARP includes real property that is, situated in Australia, relates to land situated in Australia – including a right, a license or a contractual right over land, or relates to a thing or combination of things fixed or installed on land situated in Australia. The clarification regarding “real property” is proposed to apply retrospectively from 12 December 2006.

- Amended Principal Asset Test – 365 day test period: For indirect interests in TARP, the point in time Principal Asset Test is amended to a 365-day test period. The Principal Asset Test is satisfied if the underlying entity derived more than 50% of its market value from TARP, at any time during 365 days that precede the CGT event happening.

- An introduction of a new capital gains tax 50% discount for foreign resident taxpayer who dispose of Australian renewable energy assets. The renewable energy concession is proposed to apply from the first day of the next quarter following Royal Assent until 30 June 2030.

- Foreign resident vendor – sale of shares or other membership interest – a new notification obligation to the ATO – where sale proceeds is greater than A$50 million

Further consultation regarding some of the above measures will occur from May 2026.

Global and domestic minimum tax – 15% minimum tax rate to large companies

The Budget confirms the Government will amend Australia’s global and domestic minimum tax legislation to implement the OECD/G20 Inclusive Framework “side-by-side package” agreed on 5 January 2026.

The amendments introduce additional safe harbours and extend transitional measures intended to reduce compliance burdens and duplication for in-scope multinational enterprise groups where domestic minimum tax regimes already apply.

The amendments are intended to support the effective operation of Australia’s top-up tax framework and alignment with other implementing jurisdictions.

The amendments are proposed to apply from 1 January 2026.

Foreign investment framework reforms

The Budget announced the Government will provide $47.5 million over four years from 2026–27 and $3.9 million per annum ongoing to Treasury and the Australian Taxation Office to strengthen and streamline Australia’s foreign investment framework. The reforms include:

- A target to process low-risk foreign investment applications within 30 days from 1 January 2027;

- Removal of ineffective conditions on existing approvals;

- Reforms to foreign investment laws; and

- Reforms to the Register of Foreign Ownership of Australian Assets.

Foreign residential property acquisition restrictions

The Government announced an extension of the temporary prohibition on foreign investors acquiring established residential dwellings until 30 June 2029. The ban was originally introduced for two years from 1 April 2025.

If you have any questions about any of the Budget announcements and what they mean for you or your business, talk to your trusted Nexia Advisor.

Australian Federal Budget Insights 2026/27

Download PDF